The Real Fetaverse

The Real Fetaverse

Greece's most competitive market: Feta

In this post, we're temporarily shifting away from our usual stock market discussions to pay homage to the market that inspired the name of our publication: Feta.

Feta isn't just a cheese; it's deeply ingrained in Greek culture and holds a special legal designation known as Protected Designation of Origin (PDO). This status, akin to Champagne in France, signifies that genuine Feta can only be produced within specific geographical boundaries and must adhere to strict guidelines.

This recognition was earned in 2002 and since, has faced legal headwinds, including a notable one against Denmark, to establish Greece's rights to the "Feta" name.

Beyond our appreciation for Feta's unique qualities, let's delve into the market's potential. The “Fetaverse” is forecasted to achieve a market value of $15.6 billion by 2028, as indicated by certain research.

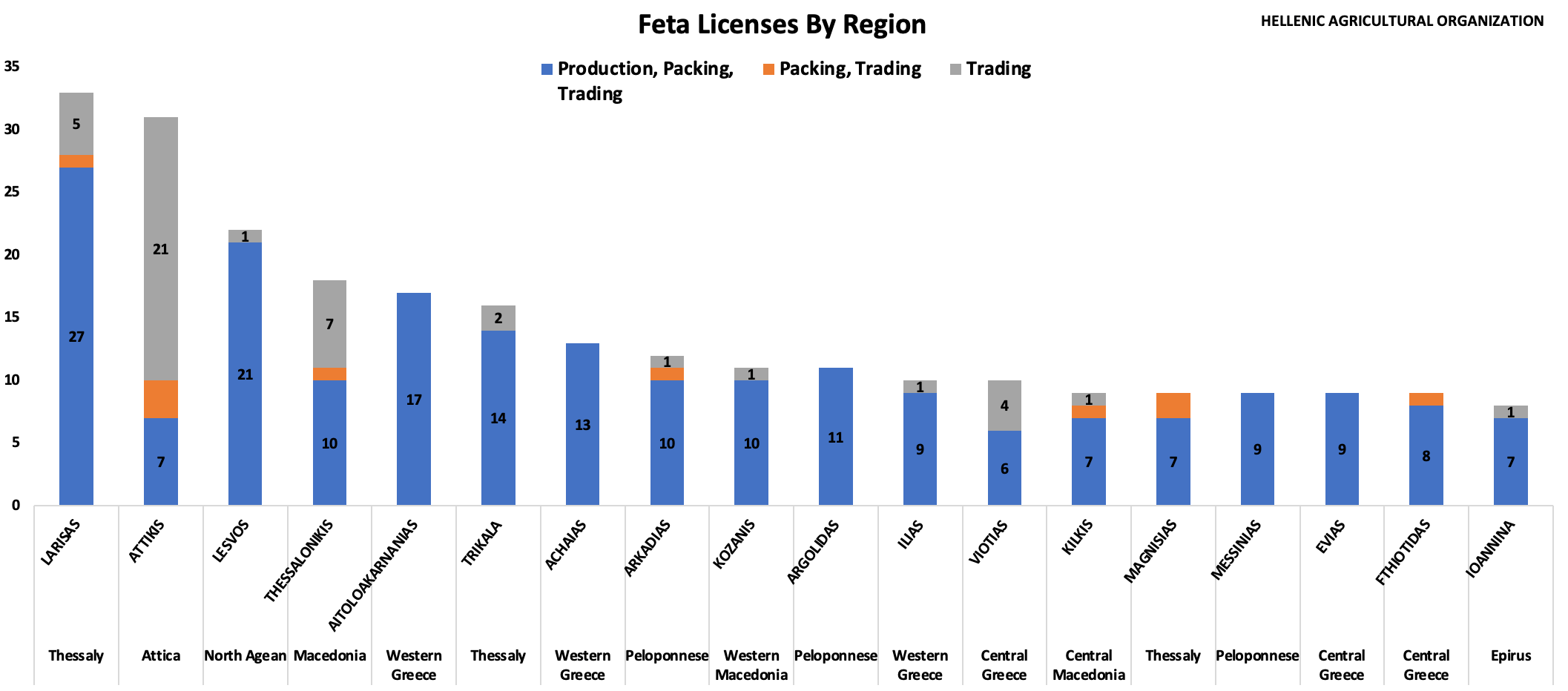

Having set the geographical context, let's focus on the participants. Feta can only be made within specific regions in Greece, including Thrace, Macedonia, Epirus, Thessaly, Central Greece, Peloponnese, and Lesvos. Furthermore, the goat’s milk used must originate from designated areas and meet specific standards.

Currently, Greece has issued 329 PDO Feta licenses for various aspects like production, packaging, or trading/distribution. Among them, only 263 are dedicated to production, while the rest cover a range of non-production services. The list spans from well-known brands like Dodonis, Epirus, and MEVGAL, to smaller local farm operations.

Securing the license to produce Feta is no easy task, even meeting the right criteria doesn't guarantee a license. They are limited and often only become available when a current licensee is relinquished or suspended. Additionally, as with many things in Greece, its takes some political ju-jitsu and influence.

Let's delve into more specifics and break down the distribution of licenses by prefecture. Larissa leads, representing almost 10% of the total licenses. The Attiki region, which encompasses Athens, also holds a substantial number, though most pertain to distribution rather than production. Lesvos stands as the second-largest producer, boasting 21 licenses. In a country that produces around 120,000 tons of Feta per year, the competition is fierce in the face of a limited number of licenses.

The pricing landscape is a battleground, with brands striving to offer the most enticing deals to consumers. Larger brands tend to have an advantage in distribution networks, both locally and globally, as well as being able to meet large super market delivery orders. This dynamic not only influences shelf prominence but also accessibility, as consumers come face-to-face with recognizable names during their shopping trips at the largest super markets. A past press release from Epiros Feta indicated they alone account for a 15% market share in Greece.

Greek Super market websites:

In summary, the Feta market encapsulates a blend of cultural heritage, legal protection, and intense market dynamics. The PDO designation underscores Feta's exclusivity to specific Greek regions and standards. As a market, it holds promise, with a projected value of $15.6 billion by 2028. Yet, behind the scenes, securing a license isn’t easy as its involves navigating certain criteria and limited availability. Supermarket competition adds another layer, with pricing wars and distribution advantages favoring larger brands.

Before we conclude, here's one final nod - an old music video that might get stuck in your head all day.

Don't mess with my Feta! ;)

FETA is unique, hence there is only one: FetaRealVerse ;)