My Not So Big Fat Greek Yield

My Not So Big Fat Greek Yield

Greek Bank Deposits Are Earning Less Than European Average

This post outlines the current state of Greek households' reliance on bank deposits, the challenges they face with interest rates moving higher, and the lack of alternative investment options and tools.

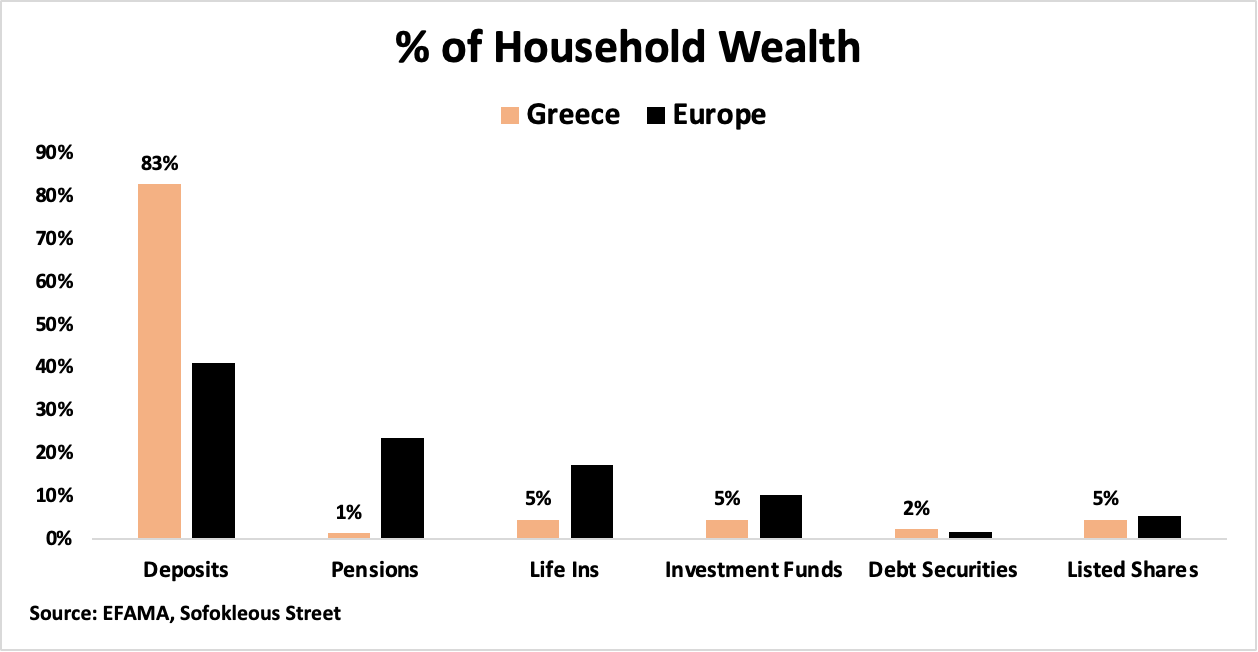

In Greece, households hold the largest portion of their assets in bank deposits. Over 80% of Greek household assets are kept in bank deposits, which is significantly higher than the European average. However, these deposits earn less interest compared to other European countries. According to the Bank of Greece, the average deposit rate being paid to households .53%.

Why Are Greek Deposits Earning Less?

One key reason for the lower interest rates is that Greek deposit accounts are not particularly sensitive to rate changes. This is because these accounts are primarily used to pay bills and other short term expenses Additionally, Greek households generally lack familiarity with alternative high yield saving options, making them less likely to leave and seek other investments.

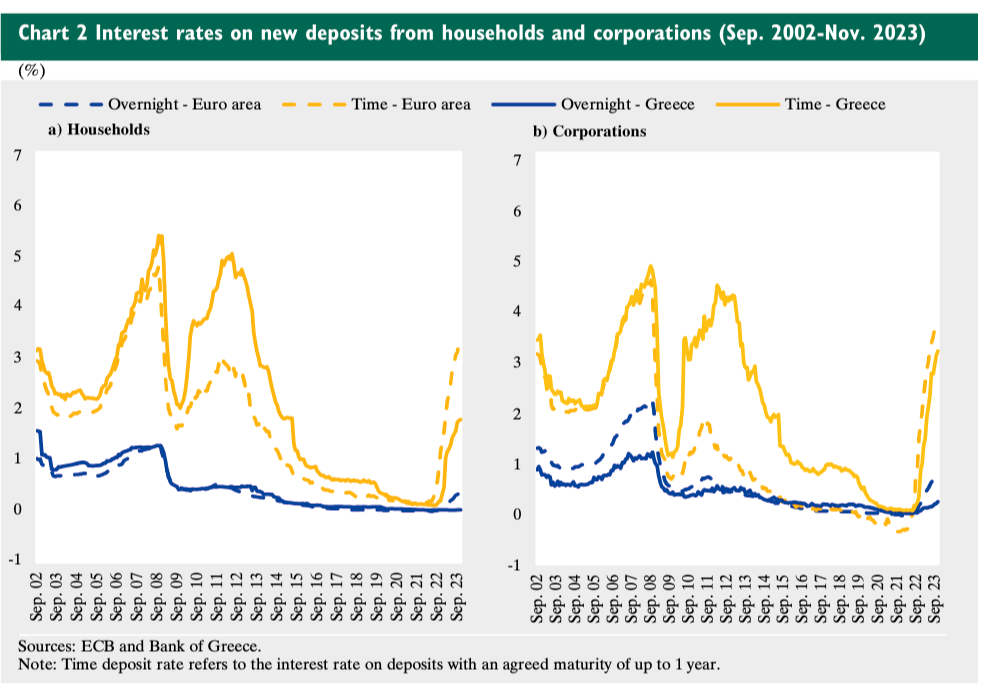

The Bank of Greece conducted research that shows how banks pass through higher interest rates to their depositors (Greece in yellow). While global interest rates have risen, Greece passes through less of these increases to its depositors compared to the rest of Europe. Historically, Greece had outpaced Europe in this regard, but this trend has reversed. This issue is common across banks globally as they aim to avoid or prolong paying out higher interest rates for as long as possible. Greek households are particularly affected due to their heavy reliance on savings accounts.

Limited Competition

Another contributing factor is the limited number of major banks in Greece—only four. This lack of competition does not incentivize banks to increase their interest payments. Additionally, there is a scarcity of electronic investing platforms that would allow for easy transfer of funds between accounts.

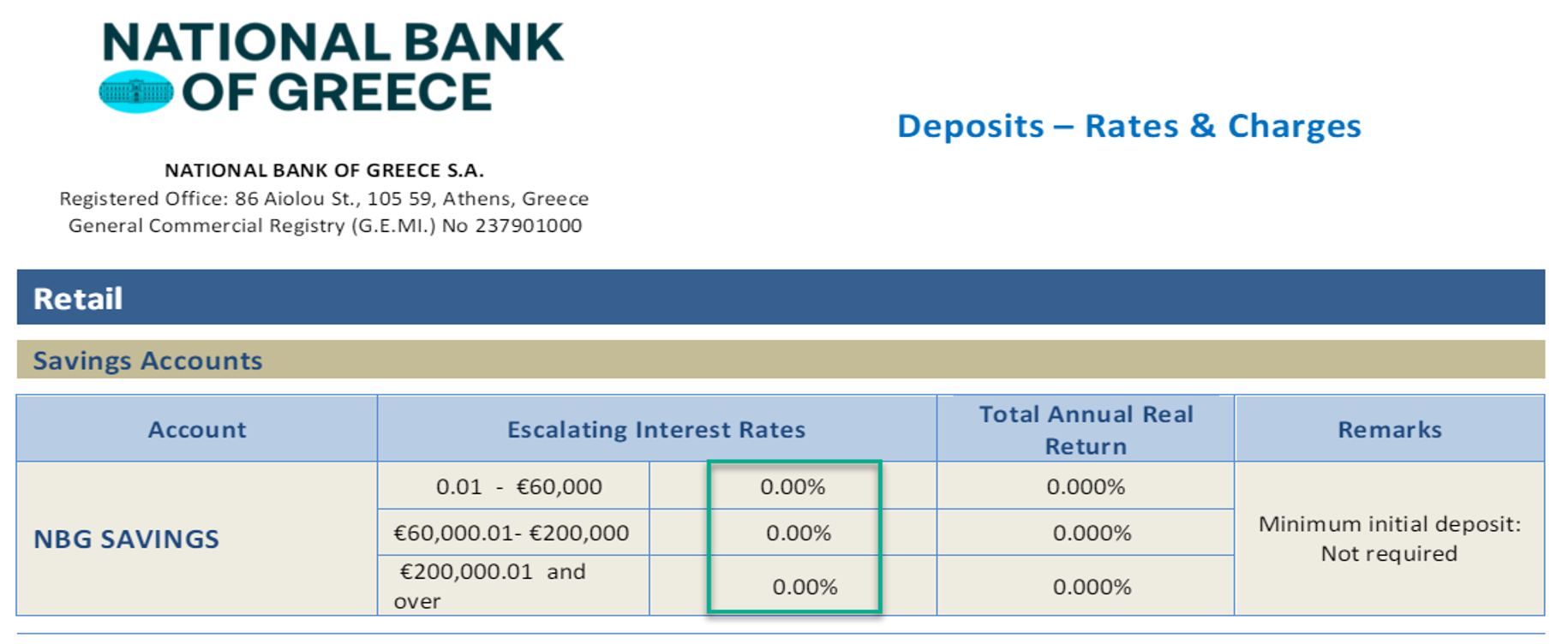

Here's a schedule from the National Bank of Greece showing the interest paid on balances to retail depositors. As you can see, the rate is essentially zero. There are higher-yielding options available, such as time deposit accounts, but these require a higher minimum investment. A customer needs a minimum of €100,000 to earn over 1.7%. Unfortunately, this is out of reach for many, as more than half of household deposits in Greece have balances of less than €50,000, according to Bank of Greece research.

Lack of Investment Apps and Alternatives

Greece also lacks investing apps that make it easy for households to transfer money and invest in short-term vehicles to generate more yield. For example, Betterment, an electronic robo-advisor in the US, offers high-yield savings options and allows customers to buy money market mutual funds or ETFs.

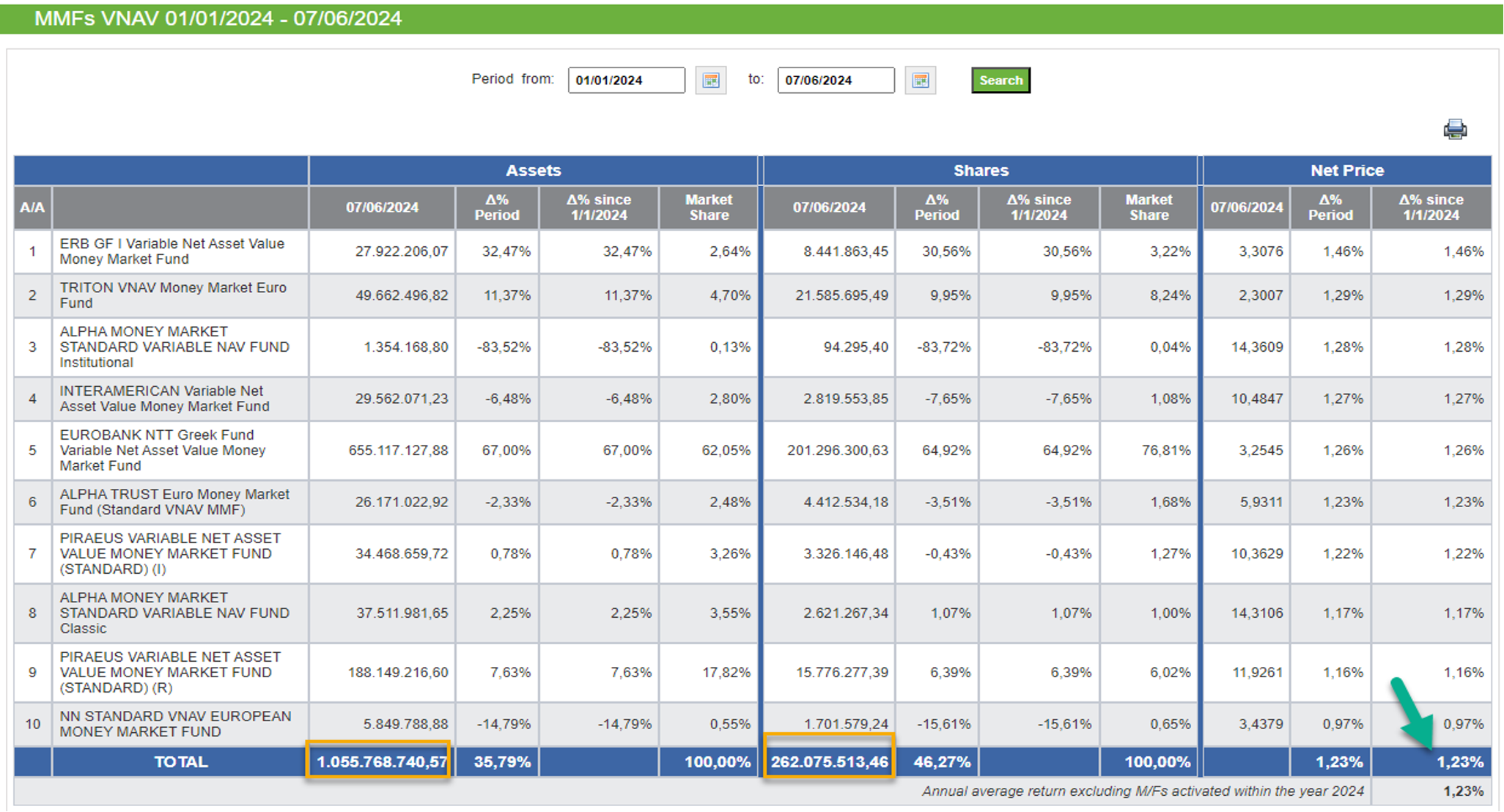

Money market mutual funds (MMFs) do exist in Greece and have been attracting more sophisticated investors in search of higher yields. Data from the Hellenic Fund and Asset Management Association shows that these MMF funds have over €1 billion in assets, and so far in 2024, they have returned an average of 1.23%, which could reach nearly 3% annually. However, to invest in these funds, Greek investors must have an investment account, which many do not. Only 10% of the Greek population has any sort of investment account. One advantage of these funds is that they have no minimum investment balance or lock-up period.

For comparison, in the United States, data from FRED shows a massive spike in money moving towards money market funds as interest rates increased. These funds have a balance of over $6 trillion.

A short-term 3-month Greek bond is currently yielding near 4%. The potential for higher returns exists if Greek households had more access to and knowledge about alternative investment options.

We need to talk more openly about this in Greece.

I do hope the Bank of Greece takes it seriously at some point.